Results¹ Highlights

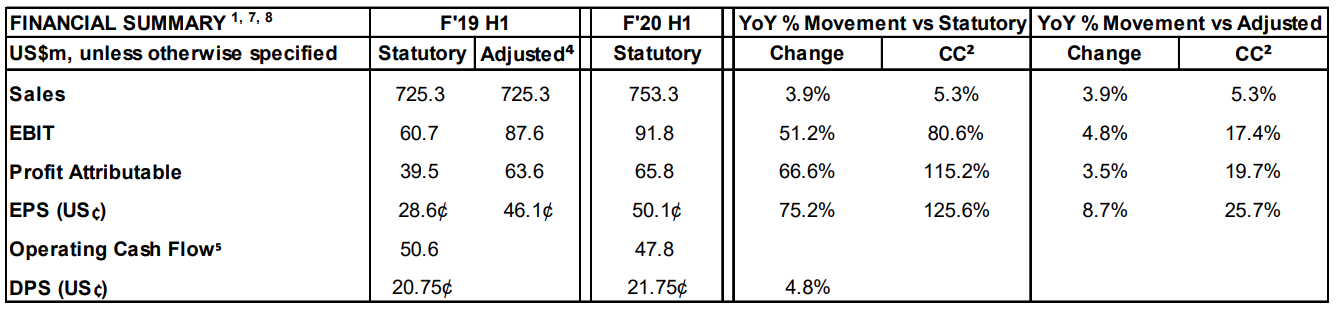

(Please note all amounts in this release are reported in US dollars)- Sales of $753.3m; 3.9% growth, 5.3% Constant Currency (CC)² and 2.4% organic growth³

- Healthcare organic growth³ of 3.4%, solid momentum maintained

- Industrial organic growth³ of 1.3%, EMEA recovery and continued APAC growth

- EBIT of $91.8m, up 4.8% YOY and 17.4% on CC vs F’19 H1 Adjusted EBIT⁴

- Profit Attributable of $65.8m, up 3.5% YOY vs F’19 H1 Adjusted Profit Attributable⁴

- EPS of US50.1¢, up 8.7% YoY and 25.7% on CC vs F’19 H1 Adjusted EPS⁴ due to sales growth, transformation benefits, favourable raw material costs and share buyback. FX a headwind

- Strong Operating Cash Flow generation of $47.8m⁵ and Cash Conversion of 92.9%⁶

- Increased half year dividend to US21.75¢, 4.8% growth over F’19 H1

1. F’20 H1 P&L results are NOT adjusted; F’19 H1 P&L results were adjusted for costs of Transformation Program

2. Constant Currency (CC) compares F’20 H1 to F’19 H1 results restated at F’20 H1 average FX rates; See Slide 34 of F’20 H1 Investor Presentation.

3. Organic growth compares F’20 H1 to F’19 H1 revenue at Constant Currency (see above) and excludes the effects of acquisitions.

4. F’19 H1 Adjusted EBIT, Profit Attributable and EPS excludes transformation costs. See Slide 31 of F’20 H1 Investor Presentation for further details.

5. Operating Cash Flow defined as Net Receipts from Operations per the Consolidated Statement of Cash Flows adjusted for net expenditure on property, plant, equipment, intangible assets, lease repayments, net interest and tax. See Slide 23 of F’20 H1 Investor Presentation.

6. Cash Conversion calculated based on Net Receipts from Operations over EBITDA (adjusted for full year incentives & insurance payments paid in H1).

7. F’20 H1 financial information prepared under AASB 16: Leases, F’19 H1 financial information prepared under AASB 117: Leases.

8. Ansell’s financial results are reported under International Financial Reporting Standards (IFRS). This release includes certain non-IFRS measures including Adjusted EBIT, Profit Attributable and EPS, and EBITDA, Operating Cash Flow, organic growth and constant currency. These measures are presented to enable understanding of the underlying performance of the Company without the impact of non-trading items and foreign currency impacts.

Non IFRS measures have not been subject to audit or review.

Comments by Ansell Chairman, John Bevan

“In a half year where geopolitical tensions continued to impact global economies, sectors and business sentiments, Ansell delivered solid sales, earnings growth and strong cash generation; again, a demonstration of the resilience of its diverse business operations and disciplined execution of its strategy. Ansell continues to build its competitive advantage and future growth potential by strengthening its manufacturing prowess and moving towards higher productivity and level of automation. We are well positioned to support growth above market rates with enhanced operations including the large Thailand plant expansion well underway and additional production capacity being added at other Ansell facilities. M&A assessment remains an active undertaking supplemented by a well-disciplined due diligence approach.

As approved at the 2019 AGM, we have an ongoing share buyback program that resulted in $40m of shares repurchased during F’20 H1. Since the announcement of the Sexual Wellness GBU divestment, the company has deployed $312.4m in repurchases of 17.7m shares to further shareholder returns. This represents a buyback of 12% of issued stock over that time period. The company expects to continue capital deployment on a combination of acquisitions, share buybacks and manufacturing capital investments for organic growth. For F’20 H1, we are pleased to declare an interim dividend of US21.75¢ which is an 4.8% increase compared to the prior corresponding period. We are confident that for F’20, we will be able to deliver our 17th year of increased dividends demonstrating the strong and sustained cash flow generation of Ansell’s business.’’

Business Review – Comments by Ansell CEO and Managing Director, Magnus Nicolin

“We entered this fiscal period facing trade uncertainties, a weaker macroeconomic environment and challenges in some key markets. The continued focus on successful execution of strategic priorities and the benefits of portfolio diversification enabled Ansell to deliver solid financial results and positive organic growth of 2.4%.

While the Industrial GBU performance of 1.3% organic growth is a little short of our expectations, we were encouraged by the sales recovery in EMEA and continued expansion in APAC. We are confident that the Industrial GBU will deliver on its accelerated growth trajectory as the economy continues to recover.

The integration of the Ringers business is progressing well with comparable sales growth of 13.5%. We’ve expanded the reach of this best-in-class portfolio of impact protection gloves into Ansell’s global markets and customers in EMEA and APAC.

Our Healthcare business continued its positive momentum delivering organic sales growth of 3.4% with improved profitability. We are pleased with the strengthening of our market position and increased traction of our innovative products, most notably the HiChem® Single use multilayer platform which grew at +70%. We are also delighted with Surgical & Safety Solutions delivering 5.8% organic growth. We are continuing to see benefits from our sales strategy in tailored product solutions, improved penetration in North America and additional investment in emerging market sales resources. Life Science had another strong performance achieving 9.5% growth propelled by the continued success of the Nitritex acquisition. Exam / Single Use continues to achieve good growth with a robust pipeline to drive sustainable growth in future periods.

We currently expect the coronavirus crisis to have both positive and negative impacts on Ansell’s business. We are actively supporting the Chinese authorities to provide a significant amount of personal protective equipment (PPE) which has increased demand for these products. We also expect negative effects due to broader external plant shutdowns in the manufacturing sector, decreased manufacturing production, lower stock levels and potential supply chain disruption which may also have some adverse implications for our customers. Overall, we anticipate that the coronavirus crisis will have a minimal net impact to Ansell’s F’20 financial results. We are working hard to support Chinese authorities in

combatting this virus and to minimise any supply disruption to our customers.

Ansell remains committed to leading the PPE and Healthcare industries in terms of Sustainability and labour practices in relation to our own plants and we continue to work closely with our suppliers to ensure appropriate labour standards are being employed throughout our supply chain.

Overall, I am pleased with the progress achieved in the business over the half year period. Across the Group’s portfolio, our strategy, new innovative products, emerging market opportunities and benefits from recent acquisitions position us well to drive sustainable growth, deliver on our financial expectations while providing the best safety solutions to our customers.”

Global Business Unit Performance

Healthcare GBU – 52.4% of revenue and 59.5% of Segment EBIT

Sales grew 4.1% in constant currency and 3.1% on a reported basis including six months contribution from Digitcare, which was acquired in October 2018. Organic growth was up 3.4%. Emerging markets continue to perform strongly with 7.1% growth and new product sales remain strong with 13.7% contribution.Life Science and Surgical & Safety Solutions continue to perform well with 9.5% and 5.8% organic growth, respectively. Surgical & Safety Solutions maintained its migration towards synthetic surgical products offsetting a decrease in lower margin powdered surgical gloves. Life Science continued to expand with its salesforce and partnerships. Exam/Single Use sales increased 1.4%.

EBIT in constant currency was 26.4% higher than the prior year. This was due to favourable raw material costs, particularly nitrile, as well as improved manufacturing performance and benefits from pricing initiatives. Currency was a negative headwind, and on a reported basis, EBIT was up 14.0%.

Industrial GBU – 47.6% of revenue and 48.4% of Segment EBIT

Sales increased 6.5% in constant currency and 4.7% on reported basis including six months contribution from Ringers, which was acquired in February 2019. Organic growth was up 1.3%. Despite ongoing challenges persisting in the automobile sector, performance has improved over the prior corresponding period and EMEA saw a strong recovery with 5.1% growth. APAC growth remained elevated predominately due to China. US and Mexico performance were lower than anticipated as a result of reduced business confidence and economic uncertainty.Mechanical sales growth was 0.5%, an improvement over the prior corresponding period but remains weaker than desired in a soft industrial market. Despite this, Ringers® and EDGE® has helped to drive growth due to strong demand for these products. Chemical sales growth was 3.0%, predominately due to a customer restocking on retail household gloves.

EBIT in constant currency was 11.0% higher than the prior corresponding period, due to Transformation benefits partly offset by increased labour related costs and marketing initiatives. Notably, the complexity of the Transformation program, whilst achieving operational benefits, also temporarily disrupted service levels. This has now been addressed and we still expect full delivery of transformation benefits as previously outlined. Notwithstanding underlying growth similar to the Healthcare GBU, currency was a negative headwind driving reported EBIT down 1.8%.

Currency, Cash Flow and Financing

The net impact of currency movements during the period was unfavourable to revenues and EBIT by $9.7m and $9.1m respectively. This is primarily due to the weakening of the Euro vs USD, which has a higher revenue than cost contribution and improving THB vs USD which is predominately a cost currency. In addition, F’20 H1 net foreign exchange gain was $1.5m vs the prior year of $2.8m.Cash conversion was 92.9% after adjusting for incentive and insurance payments which were paid in H1 for the full year. Operating cash flow generation was $47.8m. This was lower than last year’s $50.6m by 5.5% due to higher capex as the company continued to invest in projects for growth and profitability improvements. This included the commencement of a $32m investment in Thailand over two years to increase plant capacity by 30% to address the growing demand for Ansell’s chemical protection platform products.

During F’20 H1, Ansell purchased 2.1m shares on market at a cost $40.1m. The Company’s net debt: EBITDA ratio of 1.0x, remains well below targeted leverage ratio levels. Strong liquidity allows flexibility for a continuation of share buybacks, accelerated capital investment and value accretive M&A.

Dividend

An Interim Dividend of US21.75¢ (US20.75¢ F’19 H1) per share has been declared. This is a 4.8% increase on the prior year demonstrating confidence in Ansell to continue to generate strong cash flows, while maintaining significant funding capacity for growth initiatives. The record date will be the 25th February, 2020 and the payment date the 12th March, 2020. For non-resident shareholders, the dividend will not attract withholding tax as it is sourced entirely from the Company’s Conduit Foreign Income Account.Dividend Reinvestment Plan (DRP)

The DRP will be available to resident shareholders of Australia, New Zealand and the United Kingdom with an election cutoff date of 26th February, 2020. The pricing period will be based on the trading days commencing 28th February, 2020 and ceasing on 5th March, 2020. No discount will be available.F’20 Outlook

In the second half of calendar 2019, there were continued uncertainties around global economies and trade. There are now tentative signs that global growth may be stabilising, though at subdued levels. The overall financial implications of Coronavirus are difficult to predict and anticipated to be minimal at this time.Given our views on pipeline and strategic initiatives underway, we maintain our F’20 EPS guidance range 112¢ to 122¢ compared to F’19 adjusted full year EPS of 111.5¢.

ENDS